.jpg?height=120&name=LendingPad_nobigdot_ver2%20(6).jpg)

RMLA is only supported format: Residential Mortgage Loan Activity (RMLA) – This component collects application, closed loan, individual mortgage loan originator (MLO), Line of Credit, servicing, and repurchase information by state

To obtain regulatory reports and to file call report, please

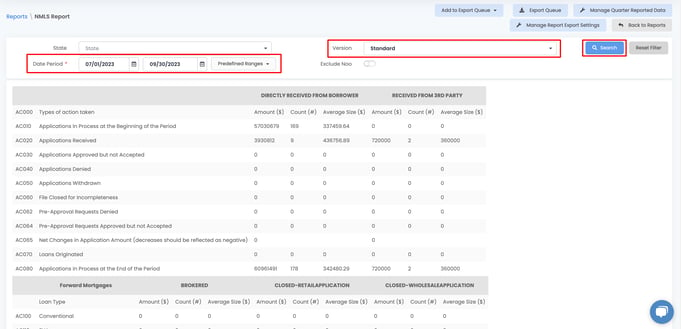

- Log into the application. Go to the "Report" menu, and search for "NMLS (MCR) Report".

- Select State in the State drop-down (for confirmation purposes only) menu or leave it blank to report for all states originated.

- Select Date Period from the calendar drop-down menus for "From" and "To" periods.

- LendingPad will determine the correct version based on your subscription to Lender, Broker, or Wholesale.

- Exclude NOO option will allow you to exclude all loans with investment purposes from the report.

- Select Search. NMLS formatted data will appear.

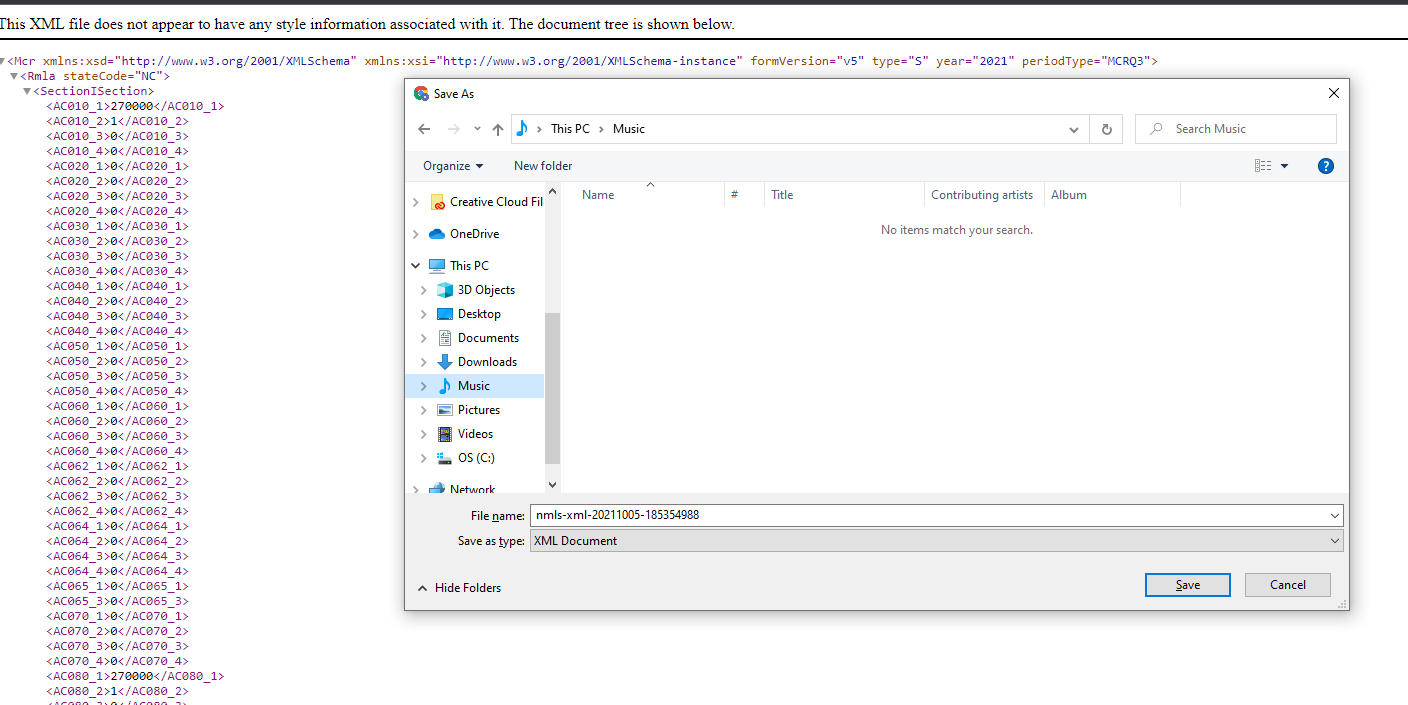

Click on "Add to Export Queue" button and select XML to export the report to XML.

Then click "Export Queue" and click on Download once the report is out of Pending status.

After clicking on the download button, a new tab will open with the XML report, In order to save this XML file into your system Press Ctrl+S(Windows) or Command+S(Mac) on your keyboard.

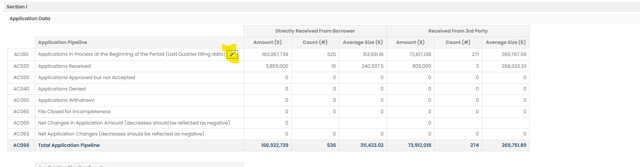

There is a "Manage Quarter Reported Data" option available next to the "Export Queue" option. If you enter prior quarter's reported data for the states you operate in, the system will auto-calculate next quarter's AC065 line. Use the Search button again to recalculate the data.

To use these reports correctly, please make sure there is a process in place with your operations team or processors to ensure data integrity and specifically, check the following data points:

- The company must have license information completed in Settings for each state they are licensed in.

- Subject Property State must have value for each loan file to be reported. If it's not there, the system cannot report this loan file as NMLS is state-specific.

- Loan's program must be selected.

- Application Taken Date (this date must exist on every loan for all reporting)

- Approved Date / Suspended Date / Clear-to-Close Date (for brokers, make sure you select a lender)

- Closed Date, Funded Date

- Adverse Actions: Withdrawn Date, Not Accepted Date, Incomplete Date, Cancelled Date, Denial Date, Rescinded Date

- For preapproval loans, please be sure to log the detail in Additional / HMDA / Action Date, Action Type drop-down - "Preapproval Approved But Not Accepted" or "Preapproval Denied".

- Always export a copy of the spreadsheet (excel) at the time of XML file download / NMLS submission as a backup record

- After you upload the XML file, please be sure to review each item for accuracy on the report before submission to NMLS.

- Timely withdrawal / adverse action files (recommended within 90 days) is recommended

- For non-qm loans please go to the Loan Additional > Compliance Information section and toggle on Non-Qualified Mortgage toggle.

To display the broker fees on the call report correctly, follow either of these steps:

- Input the compensation amount under the loan lock information section

- In the Disclosure / Fees screen, set fees "Paid To" type to "Broker" and input the fees

- AC1100 is now aligned to AC600 calculation. Before 11/9/2020, AC600 displayed the total amount of broker fees, the sum of LPC or BPC, and AC1100 pulled all fees paid to "Broker" as labeled in Disclosure/Cost Detail screen

- For retail lenders or lenders with partial broker operations, AC1100 = AC600 + AC610 + any Gain on Sale (over par) for loans sold during that period. It includes all the fees that are "Paid to Lender" in the Disclosure screen for retail banked loans and all brokered loans' LPC/BPC premiums. Before 11/11/2021, AC1100 was calculated with the total of AC600 and AC610 only and clients were advised to add the secondary gain manually.

Always consult with your own compliance resources as compliance interpretations may be different in each case. This article is provided for reference only.

Related articles

NMLS Call Report Definition

Version V6: NMLS V6 definitions

Broker YouTube Video: